The economic trajectories of South Korea and Taiwan are increasingly diverging. While the figures from the International Monetary Fund (IMF) may seem dry, their implications are significant. Last year, South Korea fell behind Taiwan in per capita Gross Domestic Product (GDP) for the first time in 22 years. This trend is expected to continue, with projections suggesting that by 2031, the gap will widen to over $10,000.

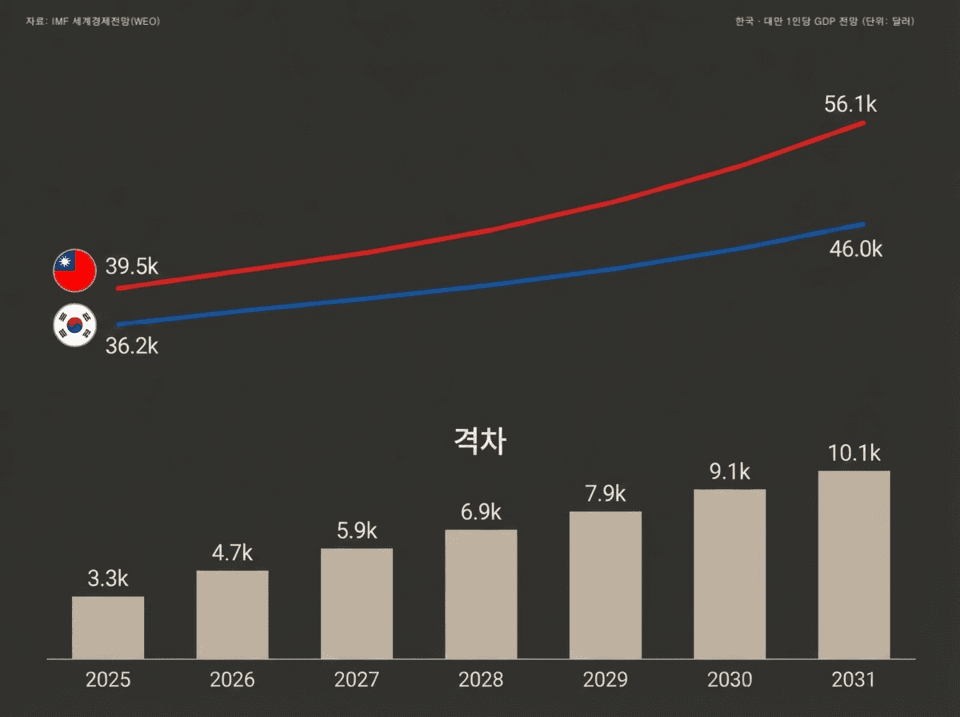

The IMF, in its recent “World Economic Outlook” report released on the 14th of this month, projected South Korea’s per capita GDP to be $37,412 this year—an increase of 3.3% from last year’s $36,227. During the same period, Taiwan’s GDP is set to grow from $39,489 to $42,103, surpassing the $40,000 mark earlier than South Korea.

While the numbers may appear mundane, the underlying structure is exceptional. South Korea is expected to reach $40,000 by 2028, while Taiwan is projected to enter the $50,000 range by 2029, not only lagging by two years but also solidifying a lead rather than catching up.

Each year, the gap widens, and the turnaround becomes more distant. Forecasts by the IMF clearly illustrate Taiwan’s accelerated growth. The per capita GDP gap between the two countries starts at $4,691 this year, expanding to $5,880 by 2027, $6,881 by 2028, $7,916 by 2029, and $9,073 by 2030. By 2031, South Korea’s per capita GDP will be $46,019, while Taiwan’s will reach $56,100, marking a gap of $10,081.

The same trend is observed in the global rankings. South Korea is expected to drop from 40th place this year to 41st by 2031, while Taiwan climbs from 32nd to 30th. The gap between the two countries will widen to 11 places by 2031.

These figures indicate that it’s not merely a race to catch up, but a decisive closing off of potential re-overtake. Compared to last October’s projections, South Korea’s per capita GDP forecast for this year has been downwardly adjusted by about $100. This is the result of the dollar-converted indicator being reduced due to the depreciation of the Korean won. While the exchange rate veils structural weaknesses, Taiwan is accelerating in the opposite direction.

Even when compared with Japan, South Korea’s position seems precarious. The IMF projected Japan’s per capita GDP for this year to be $35,703, which is a slight decrease from last year. Japan is not expected to surpass $40,000 until 2029 and will remain at a similar level as South Korea afterward. While South Korea and Japan tread on each other’s shadows, Taiwan has already moved into a different league.

The rapid rise of Taiwan is not accidental. Its manufacturing base is inherently different from that of South Korea. Last year, manufacturing accounted for 35.2% of Taiwan’s GDP, 6.4 percentage points higher than South Korea’s 28.8%. Within this manufacturing sector, the value-added share of semiconductors and electronics reaches 57.5%, which is 2.5 times higher than South Korea’s 23%.

These structural numbers reveal where a country’s growth engine is concentrated. Although Taiwan has been criticized for its excessive reliance on a single company, TSMC, this concentration is proving to be a strength in the era of artificial intelligence (AI).

By expanding its 2nm process and investing in advanced packaging, TSMC has solidified its position in the global foundry market. The AI chip supply chain from NVIDIA to TSMC is boosting the entire Taiwanese economy. The Taiwanese government has supported TSMC by prioritizing the allocation of electricity and industrial water.

South Korea also possesses a semiconductor industry, but its dependence structure is different. It focuses on memory semiconductors, and its export industries are more diversified. While this is an advantage, it is a limiting factor on growth in a situation where the AI boom is focused on specific technology segments. Both countries are semiconductor powerhouses, but who can capture the emerging market more significantly is evolving.

The five-year forecast by the IMF does not depict a predetermined future. It’s a picture that will emerge if current trends persist. The figures are subject to change depending on factors like the continuation of the semiconductor boom, the sustainability of the AI investment boom, and exchange rate fluctuations.

South Korea’s tasks are clear. The key lies in how robustly it can build its high-value-added manufacturing sector. Securing irreplaceable areas within the global supply chain, such as AI semiconductors, foundries, and advanced materials, components, and equipment, is crucial. Additionally, it is about how quickly South Korea can establish recently emerging new growth pillars like bio, secondary batteries, and defense industries.

When South Korea surpassed Taiwan in 2003, no one could predict that the gap would persist for 22 years. Likewise, the current reversal could always be turned around again. How well South Korea can build a new growth axis beyond semiconductors in the changing industrial landscape will shape the next decade.

However, it cannot be concluded that Taiwanese society has become affluent solely based on the per capita GDP figures. The gains from growth concentrated in a single industry, semiconductors, are not evenly distributed across industries and households, an issue continuously raised within Taiwan.

The “January Economic Situation Assessment” report released by the Bank of Korea in January highlighted this point. The Bank noted, “The growth skewed towards the semiconductor industry and the low labor income distribution could intensify economic polarization in Taiwan.” Following 2024, Taiwan’s exports of information technology (IT) products, including semiconductors, more than doubled, but exports of non-IT products have remained stagnant.

Bloomberg reported in February on Taiwan’s polarization in detail. While non-managerial staff at TSMC enjoy average annual salaries of about $110,000, four times the national average, 70% of this income is channeled into savings and investments rather than consumption.

Although Taiwan’s trade surplus more than doubled to $157 billion last year, its contribution to private consumption growth is only 0.7 percentage points. Reports have suggested that by 2028, Taiwan will see the largest increase in millionaires worldwide, according to UBS projections.

The gap is even more explicit in terms of figures. According to the World Inequality Lab, the top 10% in Taiwan control 48% of the total income, while the bottom 50% share only 12%—a level of wealth concentration that surpasses that of the United States. Housing burdens are also cited as being among the highest in the world since Taiwan’s house prices exceed 15 times the median income. Even with a leading per capita GDP, the living standard felt by workers is not necessarily richer.

Taiwan is also vulnerable to external variables. TSMC alone accounts for over 30% of the Taiwan stock market’s total market capitalization. A fluctuation in TSMC’s stock price could cause the entire Taiwanese economy to shake. There are also variables such as the pressure from the U.S. under former President Donald Trump for TSMC to move 40% of its production to the States. If such a relocation materializes, Taiwan could lose approximately 20% of its corporate tax revenue, which is crucial for national defense and welfare funding.

This is not just a distant anecdote for South Korea. The Bank of Korea, in the same analysis, stated that “while not as extreme as Taiwan, South Korea is not much different.” In the first 10 days of January this year, semiconductors accounted for 29.8% of South Korea’s export value, a rise of 9.8 percentage points compared to last year’s same period.

The share of the semiconductor sector in the total market capitalization of KOSPI is also significant at 37.5%. Taiwan’s warning regarding polarization due to the focus on semiconductors can equally apply to South Korea, which is also seeing a concentration in this sector.

It is difficult to conclusively describe a country’s economic conditions based solely on a per capita GDP figure, for underlying the numbers are larger variables of distribution and structure that must also be considered when analyzing the disparities between the two countries.