After the failure of the US-Iran peace talks, the US Navy announced a blockade, and oil prices have once again surpassed $100 per barrel. The monetary authority of Singapore has shifted to tightening, stating, “The energy shock has reignited an inflationary spark.”

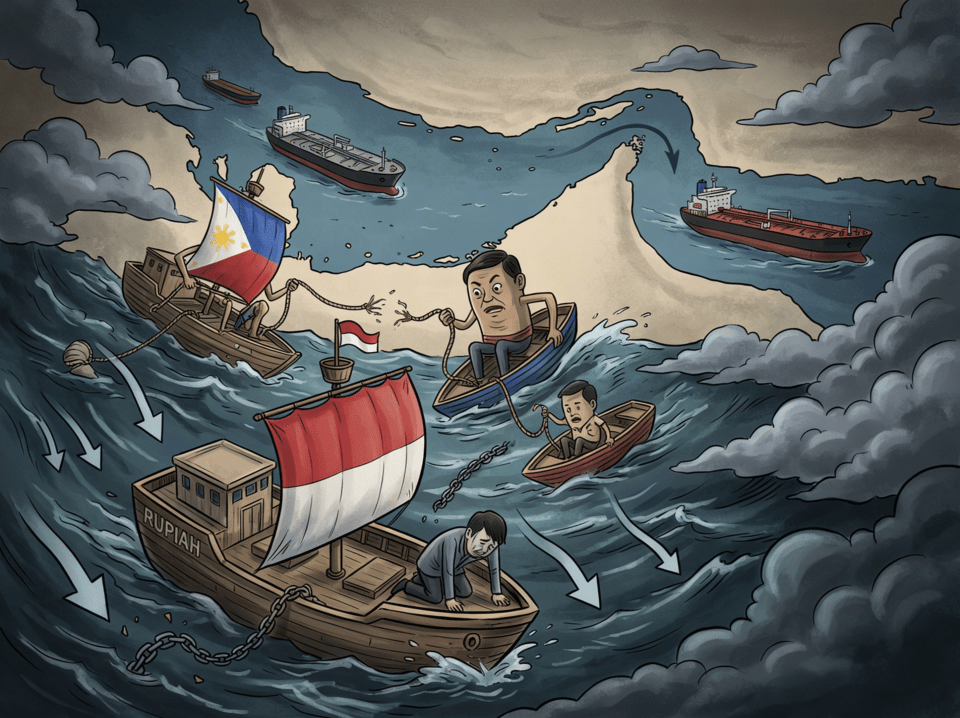

A narrow strait that carries one-fifth of the world’s crude oil is shaking up the Asian foreign exchange market. After the US declared a blockade of the Strait of Hormuz immediately following the collapse of the US-Iran peace talks, the exchange rates against the dollar fell sharply, hitting emerging countries heavily reliant on energy imports.

Negotiation failure, declaration of blockade, market shock chain reaction

In Islamabad, Pakistan, the US-Iran negotiations lasted over 21 hours before ending without agreement on the 12th (local time). Iran demanded control over the Strait of Hormuz, guaranteed rights to enrich nuclear material, and the release of frozen assets, while the US held firm on the cessation of all uranium enrichment activities and the full opening of the strait as their ‘red line.’

JD Vance, the vice president, said upon leaving, “We have presented our best and final offer.” Iranian Foreign Minister Abbas Araghchi responded, “We were very close to an agreement but hit a wall with the opponent’s excessive demands and the threat of blockade.”

Following the breakup news of the negotiations, US President Donald Trump immediately declared a naval blockade. US Central Command’s measure to cut off all ships going to and from Iranian ports came into effect at 11 PM Korean time on the 13th.

Oil prices reacted immediately. Brent crude has crossed the $100 mark per barrel again. US Energy Secretary Chris Wright predicted, “Until real ship navigation through the blockaded strait is resumed, energy prices may remain high or even rise further.”

Asian currencies were shaken in succession. The Indonesian rupiah fell to a record low of 17,135 rupiah per dollar. The Philippine peso broke the 60-peso mark against the dollar once more, and the Thai baht weakened to 32.41 baht per dollar. The Singapore dollar also slipped slightly to 1.2759 Singapore dollars per dollar.

The shock is concentrated on energy-importing countries

Michael Wan, an analyst at Mitsubishi UFJ Financial Group (MUFG), stated in a report, “The possibility of meaningful resumption of navigation through the Strait of Hormuz has significantly decreased,” and analyzed, “Currencies of energy-importing countries like the Indian rupee, Philippine peso, and Thai baht are unlikely to escape downward pressure for the time being.”

Structural weakness is revealed in the figures. As much as 84% of the crude oil and LNG passing through the Strait of Hormuz was headed for the Asian market. Since the strait was blocked at the end of February, the entire region has been exposed to the shock of supply constraints.

The Philippines, which relies 100% on imports for oil, was hit the hardest. Indonesia’s energy subsidy budget for this year was set based on $70 per barrel, and with prices over $100, the basic premise of the budget plan has already collapsed.

Weak currencies lift import prices, and the increased prices erode purchasing power again. The strong dollar accelerates this vicious cycle. As long as crude oil is traded in dollars, weakening national currencies make energy import costs more expensive. The costs in energy-intensive manufacturing and logistics sectors also rise sequentially.

Singapore becomes first in Asia to pull out the tightening card

On the 14th, the Monetary Authority of Singapore (MAS) announced in a monetary policy statement its decision to slightly increase the slope of the nominal effective exchange rate (S$NEER) policy band for the Singapore dollar. The width and central level of the band remain unchanged. It’s the first central bank in the Asian region to respond to the current energy shock with monetary tightening.

MAS stated in the announcement, “Import energy costs have already risen, and prices of more general imports and services are expected to rise over the coming quarters.” Consequently, it revised its forecast for core inflation from 1-2% to 1.5-2.5%.

The market was somewhat prepared, as 15 out of 18 economists surveyed by Bloomberg before the decision had expected tightening.

OCBC analysts had already issued a statement: “Considering the surge in oil prices and broad commodity volatility, early tightening via increasing policy slope is necessary.”

This also reveals why MAS uses the exchange rate instead of interest rates as a monetary policy tool. By rapidly appreciating the Singapore dollar, some of the increase in import prices can be absorbed by the exchange rate.

Controlling prices cools down the economy

Other countries’ central banks are in a much more complicated situation. If Indonesia’s central bank (BI) raises rates to defend the rupiah, domestic demand cools; if it holds rates steady, inflation through import prices might spiral out of control.

The concerns of the Thai central bank (BOT) are similar. Raising interest rates in the absence of a strong tourism recovery may curb the baht’s weakness but dampen economic recovery as well.

Karen Young, a researcher at Columbia University’s Global Energy Policy Center, predicted, “Even if the war ends, it’s difficult to expect oil prices to fall until the straits are reopened and the damaged oil facilities are restored,” and continued, “In some sense, high oil prices are likely to persist until the end of the year.”

Withstanding vs Diversifying

Considering the possibility of a prolonged situation, the options available to countries can be largely narrowed down to three directions:

▶ Diversifying energy sources is the most fundamental solution. Japan plans to additionally release a 20-day oil reserve, and India has resumed importing Russian crude oil under a special US permit. Discussions on expanding the introduction of Australian and US LNG to reduce Middle Eastern dependence are speeding up. The fact that countries with more dispersed sources of imports are less shocked confirms this once again.

▶ Balancing fiscal and monetary policies is a short-term measure. Randomly increasing energy subsidies disturbs fiscal stability, and rashly hiking interest rates amplifies the risk of economic recession. As Singapore has created a buffer by adjusting the slope of exchange rate appreciation, detailed policy combinations suitable to each country’s circumstances are required.

▶ The scale of foreign exchange reserves determines the thickness of the defense line. South Korea has over $400 billion, and India $688 billion in foreign reserves, providing them with some leeway to prevent rapid currency depreciation.

In contrast, countries like the Philippines and Indonesia, with thinner buffers, could be pushed to the brink faster. Although the preparation state is much better compared to the 1997 financial crisis, the longer a crisis lasts, the more that gap narrows.

Whether negotiations over the Strait of Hormuz will resume or evolve into a military conflict between the US and Iran remains uncertain. What is clear is that this strait has once again highlighted the weakest link in Asia’s energy security and currency stability. Diversifying energy sources and expanding foreign exchange defense capabilities have emerged not as choices but as matters of survival.