White House eases restrictions for bargaining, while Congress seeks to tighten them by law — U.S. policy on China is split.

If the hardline congressional plan extends the restrictions to Samsung Electronics and SK hynix plants in China, general-purpose DRAM prices could rise by an additional 22%, and NAND flash by about 10%, according to an estimate by the Korea Institute for International Economic Policy (KIEP).

Memory prices have already surged nearly fourfold in just three months. The reason is reduced supply of ordinary DRAM as production is shifted toward HBM for AI. If a policy shock is added on top of that, prices of PCs and smartphones could rise further.

Tighter controls create a backlash. Supply shortages improve the earnings of Chinese memory companies, while higher memory prices increase the cost of U.S. AI data centers.

KIEP recommends that South Korea avoid siding with either the U.S. or China and instead diversify supply chains and secure upstream technologies such as equipment and materials to spread risk.

The Biden White House and Congress are moving in opposite directions on regulations blocking the sale of advanced semiconductors to China, with the White House easing and tightening restrictions in turns while Congress pushes to harden them by law.

If the congressional hardline approach becomes reality and even the Samsung Electronics and SK hynix factories in China are blocked, memory prices, already surging, will rise further. That is the conclusion of an analysis released on the 19th by the Korea Institute for International Economic Policy (KIEP).

◆ White House loosens, Congress tightens

KIEP’s report says U.S. control policy has split into two tracks. The Trump administration’s second term uses export controls both as a security tool and as a bargaining chip. Nvidia’s AI chips for export to China are one example: sales were blocked and then allowed again, a choice intended to preserve room for negotiation.

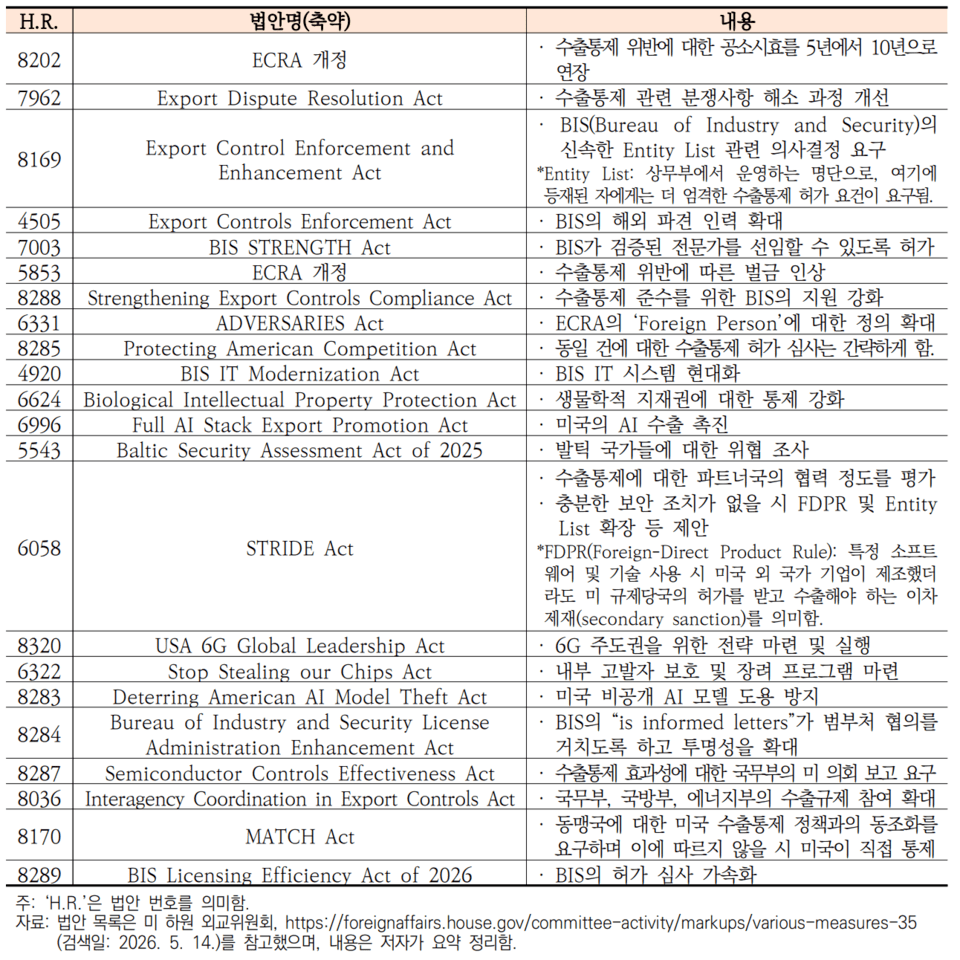

Congress is headed in the opposite direction. It believes the administration’s use of controls as leverage creates loopholes. On April 22, the U.S. House Foreign Affairs Committee passed several bipartisan export-control bills at once. While the administration remains cautious about new regulations, momentum is growing in Congress to strengthen controls on China.

One notable proposal is the MATCH Act, which would allow the United States to impose direct sanctions if Japan, the Netherlands, and South Korea do not follow U.S.-level equipment controls. Also under discussion is a bill that would tailor the intensity of controls to China’s technological level.

Export controls are measures that prevent the sale of specific technologies, equipment, or products to certain countries. The United States has continued expanding the scope of controls, viewing semiconductors as a national security asset. As the gap widens between the administration’s and Congress’s levels of strictness, the range of what companies can predict shrinks.

◆ Already a ‘DRAM fourfold’ price shock — AI is the cause

The memory market is already in emergency mode. The price of 32GB DDR5 memory for PCs has jumped nearly four times, from the 170,000-won range to around 700,000 won, in just three months. DRAM prices have risen as much as 180% from their 2025 low. The market has nicknamed this the “Ramageddon.”

The cause is AI. Samsung Electronics, SK hynix, and Micron produce ordinary DRAM and HBM on the same production lines. HBM, or high-bandwidth memory, is an advanced memory stacked in layers of DRAM for faster data processing and is used in AI semiconductors. It requires more wafer area than regular DRAM to produce each chip.

As AI demand exploded, companies increased HBM production, where the profit is. That reduced ordinary DRAM output. As supply shrank, prices surged. In other words, rising AI demand led to a concentration in HBM, and that concentration then caused a shortage of consumer DRAM.

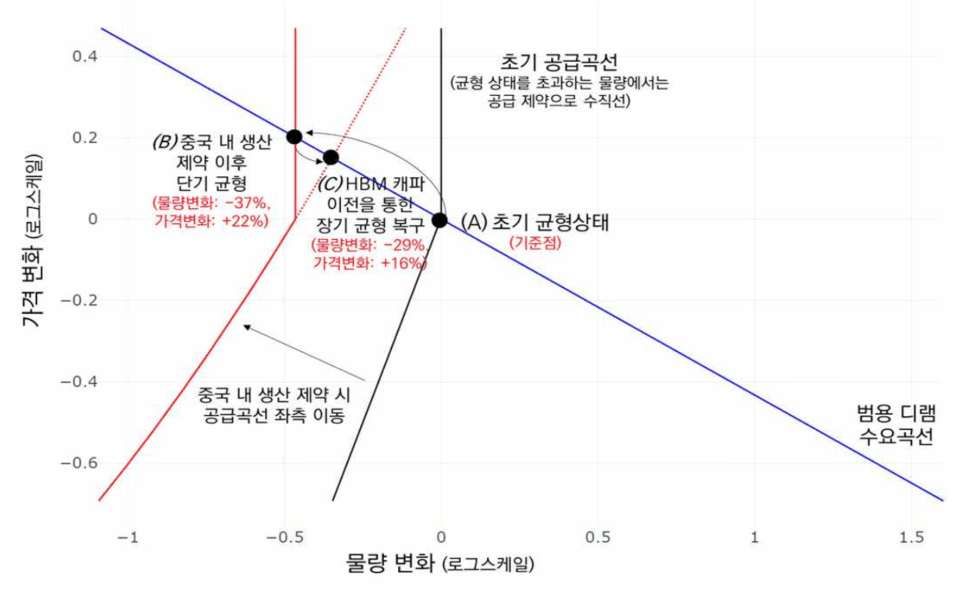

◆ If Chinese factories stop, DRAM rises another 22%

The most sensitive issue for South Korea is the factories in China. Samsung Electronics manufactures memory in Xian, while SK hynix has operations in Wuxi and Dalian. The United States has tightened pressure on China while granting exemptions to those factories, allowing existing operations but blocking new equipment imports. Hardliners in Congress want to eliminate even those exemptions.

If the exemptions disappear and the factories stop, the result will show up immediately in prices. According to KIEP’s supply-and-demand model, if South Korean factories in China halt operations, general-purpose DRAM prices would rise by about 22%, and NAND flash by around 10%, because a significant share of global memory output comes from those plants.

There is precedent. When the Wuxi plant caught fire in the past, DRAM prices rose about 40% in a single month. As soon as one plant stopped, global prices wobbled.

KIEP noted that the 22% figure is a conditional estimate based on a full shutdown assumption. Different assumptions would produce different numbers. But the direction is clear: the deeper the blockade, the larger the shock. With prices already four times higher, another policy shock could push up the cost of PCs, laptops, and smartphones.

◆ The tighter the controls, the stronger the backlash: Chinese self-sufficiency and U.S. AI costs

Stronger controls produce outcomes that run counter to their original purpose. The tighter supply becomes, the better the performance of Chinese memory companies.

Chinese firm CXMT is reportedly back in the black. That reflects both improving industry conditions and supply constraints. If the United States squeezes Korean companies’ production in China, Chinese firms will fill the gap. Rather than restraining China, the policy would accelerate its self-sufficiency.

The United States also bears the burden. HBM makes up a large share of the cost of AI semiconductors. AI data centers also require large quantities of DRAM and NAND. If controls push memory prices higher, the cost of AI infrastructure that the United States wants to expand will rise as well. In other words, a policy aimed at China ends up increasing the costs of the U.S. AI industry.

There is a clear counterargument that controls should be tightened further. With cases of advanced AI servers being smuggled out coming to light, calls to tighten enforcement have gained strength. This is where security logic and industrial-cost logic collide head-on.

◆ KIEP: Don’t side with one camp — diversify risk

KIEP’s prescription is clear. A strategy of aligning with either the United States or China is risky. If South Korea leans toward the United States, it becomes vulnerable to Chinese retaliation; if it moves closer to China, it risks additional U.S. sanctions.

The alternative is risk diversification. Production bases and supply chains should be spread across multiple countries so that if one route is blocked, the entire system does not stop. KIEP especially emphasizes upstream competitiveness. The semiconductor industry works as a vertical structure: design tools and key materials and equipment at the top, chip manufacturing below. The side that controls the top has the upper hand in negotiations. That is why the United States uses EDA design tools and China uses rare earths as leverage. Even if South Korea leads in finished memory chips, dependence on foreign equipment and materials leaves it vulnerable to a single round of controls.

The case of the Netherlands’ Nexperia offers a useful reference. The Netherlands moved in step with the United States, but even after a U.S.-China agreement, it could not easily resolve disruptions to its China business. It shows that the uncertainty of supply chains and geopolitical risk can outweigh the benefits of siding with a particular country.

Samsung Electronics and SK hynix’s factories in China have served as a buffer in U.S.-China conflict. The United States has pressured China while still granting exemptions to the two companies’ plants, and China has sanctioned U.S. firm Micron while leaving Korean companies alone. If this balance breaks, price spikes, weakened data center investment, and the rise of Chinese companies could all hit at once. That is why KIEP continues to stress risk diversification.