Hyundai Motor Company is now going beyond making electric vehicles and is moving directly into securing the minerals buried underground. By joining the development of a lithium mine in the United States, Hyundai Motor Group is accelerating its “de-Chinaization” strategy for EV battery materials.

Hyundai Engineering and the Korea Overseas Infrastructure & Urban Development Corporation (KIND) signed a letter of intent with Australian mining company Ioneer on the 23rd local time. The agreement covers joint development of the “Rhyolite Ridge” lithium-boron mine in Nevada. The LOI itself is not legally binding. The three companies plan to formalize cooperation by signing a memorandum of understanding next month.

The project is estimated at about $1.6 billion, or roughly 2.2 trillion won. The goal is to make a final investment decision in the second half of this year and begin first commercial production in 2029. Annual output is targeted at 27,800 tons of battery-grade lithium hydroxide. The company says that is enough to power about 370,000 electric vehicles. On the day of the announcement, Ioneer’s shares surged by nearly 29% intraday.

Carving out the “heart of EVs,” lithium, in the Nevada desert

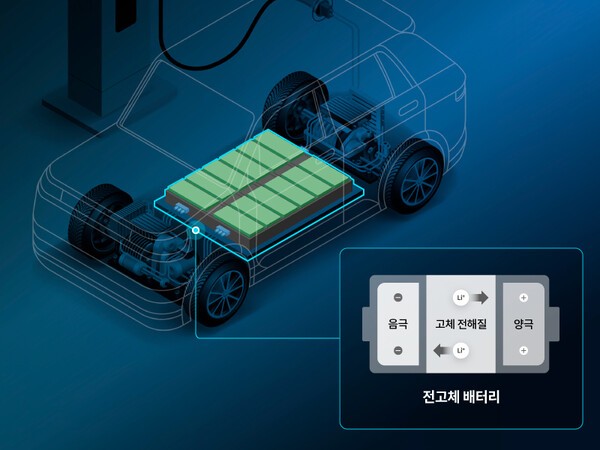

Lithium is the key raw material for EV batteries. Inside a battery, it stores and releases electricity. It is often called “white oil.” In effect, the power that moves a car comes from this mineral.

The problem is that China effectively controls the mining and processing of lithium. Dependence on China is especially high at the refining stage, when the mineral is turned into something suitable for batteries. Last year, when China tightened exports of certain critical minerals, Western supply chains were thrown into turmoil, heightening concern in the U.S. and Europe over the risk of a single country holding the supply lifeline.

That is what makes Rhyolite Ridge special. The Nevada desert mine is the only deposit in North America known to contain both lithium and boron in one place. Boron is an industrial mineral used widely in glass, ceramics, and agricultural fertilizers.

Mining two minerals from one site makes the economics sturdier. Another advantage is that the extracted ore will be processed on site into battery-grade lithium hydroxide rather than shipped to another country. The mine is located about a three-hour drive from Tesla’s Nevada battery factory, right in the middle of what is being called the “lithium belt.”

This mine did not appear overnight. Since 2016, Ioneer has poured in more than $220 million, or about 300 billion won, and has completed more than 70% of the design. Once operations begin, 275 to 300 jobs are expected to be created on site alone.

Hyundai Engineering’s role is clear. It will handle the engineering, procurement and construction (EPC) of the mine and refining plant. Its experience building large chemical and energy plants on time and within budget is a key asset. KIND will be responsible for financing the project.

Here lies Hyundai Motor Group’s strategy. In exchange for taking charge of construction, it secures bargaining power to obtain U.S.-sourced lithium from the mine in the future. Instead of buying up the mine outright, it is using “construction capability” as leverage to secure raw materials. It is a different kind of strategy from the resource-rich-country model of spending money to buy resources.

Subsidies are gone, but China-exclusion rules have become stricter

To understand Hyundai’s calculations, one must look at changes in U.S. regulations. The Inflation Reduction Act (IRA) is often the first thing that comes to mind, but the landscape has already shifted once.

At the end of September last year, the United States abolished the up to $7,500 consumer subsidy for buying an EV. A new budget law pushed by the Trump administration brought the sunset date forward by seven years. The “carrot” that made EVs cheaper to buy disappeared.

But the benefits for “making” batteries remain. Companies that produce battery cells in the United States still receive tax credits proportional to their output. There is a condition, however: if the battery contains minerals that have passed through a “country of concern” such as China, the company cannot receive the benefit. This is the FEOC rule, or foreign entity of concern rule. Consumer subsidies were reduced, but the net filtering out Chinese materials has become tighter.

Hyundai Motor has built its EV-only plant, the Metaplant, in Georgia and is making batteries there as well. If Chinese lithium is mixed into those batteries, the tax benefits at the production stage disappear. That is why securing lithium mined on U.S. soil has become not a choice but a matter of survival.

The global trend points in the same direction. The Group of Seven agreed this month in Evian, France, to reduce dependence on China for critical minerals. For rare earths and permanent magnets, it set a target of lowering dependence on any single country to below 60% by 2030. Lithium and nickel, which go into batteries, were designated as the first pilot items in new supply-chain cooperation. The entire West is turning toward “decoupling from China.”

Korean companies are moving quickly as well. Korea Zinc has unveiled a plan to build a critical minerals smelter near Nashville, Tennessee, worth about $7.4 billion, or roughly 10 trillion won. Hyundai Motor Group’s latest move is another scene in this larger wave.

From mine to finished vehicles, a Korean-led belt is taking shape

Rhyolite Ridge already bears the footprint of Korean companies. Materials company EcoPro Innovation has worked with Ioneer for years to study technology for extracting lithium hydroxide from lithium clay. Hyundai Engineering’s construction capability and Hyundai Motor’s finished-vehicle business now overlap with that effort.

Put the pieces together and the picture becomes clear: lithium is mined, refined on site, processed into battery materials by a Korean materials company, turned into cells at a Korea-linked battery plant in the United States, and installed in Hyundai EVs. It means the chain of mining, refining, materials, batteries, and finished vehicles is being linked end to end on U.S. soil. That is why the industry sees this move as a sign that a Korean EV supply chain is taking root in America.

Hyundai Engineering Vice President Lee Seung-dong said, “On the most important criteria — permitting, construction readiness, and long-term supply stability — Rhyolite Ridge is on a different level from other mineral projects,” adding, “This decision reflects the group’s determination to build a reliable critical minerals supply chain.”

There are still obstacles ahead. The mine faces environmental controversy. Local environmental groups have filed a lawsuit, saying the habitat of endangered wildflowers and native fish is under threat. That means the risk of delays remains alive.

Volatility in lithium prices is another burden. A South African mining company that had previously pledged $490 million, or about 680 billion won, to invest in the mine withdrew after lithium prices plunged. That is also why Ioneer went looking for a new Korean partner. It should not be forgotten that the latest agreement is only the first step and is not yet legally binding. A series of hurdles still remain, including next month’s MOU and a final investment decision in the second half of the year.

Still, the direction is clear. Competition in the EV era no longer ends with who makes the better car. It has shifted to a battle over who can control the uninterrupted chain from underground minerals to vehicles on the road. Hyundai Motor Group’s decision to join the first shovel in the desert mine can be read as a move to firmly anchor the front end of that long chain on U.S. soil.